What this article covers

Financial advisors don’t agree on whether seniors need life insurance — and that disagreement reveals something useful. Here’s a practical framework for deciding whether coverage makes sense for your situation, and what questions to ask before you buy.

Life insurance is a tricky subject.

It forces us to confront something most people prefer not to think about: our mortality. And as we get older, the issue feels much less theoretical.

Still, if you’re like me and already a senior, it’s a conversation you probably need to have. Should you buy life insurance late in life?

I asked several financial advisors.

- One said that seniors don’t need life insurance, and if they’re told to get one, they’re being sold expensive policies they don’t need.

- Another pointed out how the right policy can protect you from potentially devastating long-term care (LTC) costs.

- A third explained that the real question isn’t whether life insurance is right or wrong for seniors in general, but rather that you need to ask what specific financial problem it’s trying to solve.

As experts usually do, despite sharply disagreeing, they all sounded credible.

So, if even the experts disagree, how are you and I supposed to decide if buying a life insurance policy late in life is a smart move or just an expensive mistake that drains our retirement income?

This decision sits in the intersection of competing fears.

- If I buy the coverage, would I be wasting limited retirement resources on something I don’t need?

- If I decline, do I leave myself and my spouse exposed to potentially catastrophic financial consequences?

And unfortunately, there’s no universally correct answer.

I’ve wrestled with this personally because I bought term life insurance years ago for a very specific reason.

What I found was that there’s a better way to think about the decision, and good questions you can ask your financial advisor or the insurance agent you work with before making the decision for you and your family.

Key Takeaways

Most Seniors Don’t Need Life Insurance — But Some Do, for Specific Reasons

By retirement, most people have paid off debts, raised independent children, and built savings — eliminating the primary reasons life insurance exists. But for seniors with a financially dependent spouse, an LTC funding gap, estate liquidity needs, or a temporary income shortfall, the right policy can still solve a real and costly problem.

A Permanent Policy with an LTC Rider Addresses Two Late-Life Risks at Once

Unlike traditional long-term care insurance, which can reprice significantly over time, a permanent life insurance policy with an LTC rider locks in level premiums and pays a death benefit if the care rider goes unused. For couples worried about one spouse depleting their portfolio to cover extended care costs, this structure can protect the surviving partner’s financial stability.

The Right Question Isn’t Whether Life Insurance Is Good or Bad — It’s What Problem It Solves

Advisors who disagree on life insurance for seniors are usually disagreeing about which risks still matter in retirement, not about whether insurance works. Before buying any policy, identify the specific financial risk you’re addressing, confirm insurance is more cost-effective than alternatives, and make sure premiums won’t meaningfully reduce your retirement cash flow.

Why Life Insurance Decisions Get More Complicated as You Age

There’s no doubt that life insurance needs evolve as we age.

When we’re young, we may have minor children who depend on us financially, a large mortgage, limited savings, and decades of potential future income that our family will need to replace if we die.

By the time you’re a senior and retired, your kids are most likely independent adults, your mortgage may be paid off, or at least paid down to a much smaller balance, and you probably saved and invested, so your spouse would have access to (hopefully sufficient) financial resources should you pass away.

In addition, as you get older and less healthy, insurance premiums tend to rise.

In the latter scenario, continuing to pay these increasingly high premiums can start looking like a big waste of money.

Lawrence Pon, CPA/PFS, CFP®, of Pon & Associates, puts it bluntly, “Why are seniors buying life insurance besides providing hefty commissions to the insurance salespeople? You have to look at the person’s life insurance NEED. We usually have a high life insurance need when we are younger because we have not saved much money in retirement plans yet, still have a large mortgage, children are young and still need college funding, etc.”

He continues, “By the time you are a senior, hopefully your mortgage is paid off, you have saved diligently for your retirement and met your financial goals. Therefore, there is usually NO life insurance need for seniors. Their premiums will be expensive since they are older, and they have picked up a few medical conditions.

“This is pushed by the insurance salespeople. Do not waste your time or money. If you really need life insurance, find a term policy if you can find a life insurance company willing to insure you at a reasonable price. Or go get a job that comes with Group Term Life Insurance. It is a different discussion if the senior already has a policy and deciding whether to renew or not. The answer to that – it depends.”

David Demming, CFP®, of Demming Financial Services Corp., is also skeptical, noting that insurers are in the business of making money, not losing it, so these policies aren’t compelling, “Life insurance is not free, and we will all die someday. Yet insurance companies are not selling it because they expect to lose money all the time.

“Simplistically, if you can retire, your economic worth in the marketplace is now zero. Death costs are not high, unless you’re a Viking! Final expenses may require $5K-$20K. The exception is when paid by someone else or given a death sentence health call. I always remember converting a policy for a client and she lived another 15 years. Got the money back, but it was a long wait.”

Elizabeth Kusmider, CFP®, of Kusmider Consulting, adds, “At older ages, premiums can become so high that, if the insureds live many more years, they may pay more in premiums than the policy pays out. Another common (and expensive) misunderstanding is graded benefits in some final-expense/guaranteed-issue policies: for the first year or two, benefits may be limited to a return of premium or a partial payout, not the full death benefit.”

Kusmider also cautions that affordability alone doesn’t necessarily make coverage worthwhile, “Even if they can pay, it may not make sense when there’s no ongoing financial need: no dependent spouse, debts, or liquidity gap, when premiums meaningfully reduce retirement cash flow, or when the policy structure (high cost / graded benefit waiting period) provides poor value relative to simply earmarking savings.”

That skepticism resonates for many retirees, and for good reason. With less risk to protect, and higher premiums, insurance offers start sounding like we’re being sold something that generates a fat commission for the agent, and that offers us something of little value.

However, as mentioned above, some advisors see real value in life insurance coverage even late in life, especially if the price isn’t prohibitive.

When Life Insurance Still Makes Sense for Seniors

It’s clear that for most retirees, the primary purpose of life insurance is no longer replacing decades of future employment income. Instead, a policy needs to focus on protecting against late-life spending shocks, like expensive LTC, which may be hard to accomplish outside of a life insurance policy.

Raman Singh, CFP®, EA, Your Personalized CFO at Singh PWM, explains, “The biggest misconception seniors often have is to treat life insurance and LTC insurance as completely separate conversations. They are not. A permanent policy with an LTC rider addresses both risks at once, with level premiums, unlike traditional LTC policies that can reprice significantly over time, and a death benefit that pays out if the LTC rider goes unused.”

He then gives a real-world example, “I worked with a married couple in their late 60s, both retired, with a solid investment portfolio and a comfortable lifestyle. The concern that kept coming up wasn’t market risk. It was, ‘What happens if one of us needs extended care?’ Without a plan, the answer was simple and uncomfortable. They would draw down their investments to cover care costs, potentially leaving the healthy spouse with a significantly reduced portfolio and no income replacement. That is a real risk that does not show up on a balance sheet until it is too late.”

He recommended using a permanent life insurance policy with an important rider. “Instead of self-insuring that risk with assets they had spent decades building, we structured a permanent life insurance policy with an LTC rider for the higher-risk spouse. The premium stayed level, no repricing surprises down the road. If LTC is never needed, the death benefit passes to the surviving spouse or heirs. If care is needed, the LTC rider activates and the portfolio stays intact for the spouse still living at home. That is the core of risk transfer. You aren’t eliminating the possibility of needing care. You’re making sure it doesn’t financially devastate the person left behind.”

Other advisors expressed similar concerns.

Derrick Alexander, Owner and Lead Advisor of Greater Works Wealth, says, “I think the biggest misconception is only seeing the premium as an expense rather than an investment. Especially using a life insurance policy with an LTC rider.

“We had a situation where a couple was retiring, and we saw a gap in LTC planning and replacing the spouse’s social security income in the event of a premature death. The premium may be $3,000 a year for a $250k death benefit that can also be used for long-term care. Showing the client that the $250k is another bucket of cash that we are paying a discount for.

“Most people, if we were planning for a 30-year retirement, and I asked if you could pay $90k to get $250k tax-free, would say yes. If we can view it as a transfer of risk from our portfolio to a contractual agreement with an insurance company. It can help.”

Joon Um, CFP®, EA, CLU®, ChFC®, of Secure Tax & Accounting, agrees, “One of the biggest misconceptions is that life insurance for seniors never makes sense. It actually can still be very useful in your 60s and sometimes early 70s, for protecting a spouse, covering final expenses, or legacy planning. But once premiums get too high relative to retirement income, or health issues become more significant, it may simply be too expensive to justify.

“Generally, term policies work better for temporary needs, while permanent insurance is more appropriate for long-term legacy or estate planning goals, as long as they can still qualify medically and the premium makes financial sense. The most important thing is to make sure they truly understand the long-term cost before buying.”

The striking thing about these responses is that the advisors weren’t disagreeing about whether insurance works.

They were disagreeing about which risks still matter late in life, how large they are, and whether insurance is the most efficient way to handle them.

Ultimately, what they say shows that life insurance late in life can indeed solve real financial problems. But only if it isn’t overly expensive and doesn’t try to solve something that’s more effectively addressed in other ways.

Kusmider says she has seen this firsthand, “I’ve helped seniors in their 60s to mid-70s secure a modest, affordable death benefit while they were still relatively healthy. In those cases, coverage created immediate protection for a spouse, covering a mortgage payoff and end-of-life costs, so the surviving partner didn’t have to liquidate investments or rely on adult children.”

The disagreement among advisors often comes down to which risks they think retirees still face, and whether insurance is the best way to manage them, as shown in Table 1.

My Personal Experience with Life Insurance Late(r) in Life

I had to wrestle with this issue personally.

Years ago, I bought a term life insurance policy that expires when I turn 65. The reason was simple. If I died before our retirement nest egg became large enough, my wife would have been forced to sell the house and move someplace cheaper, and would have a hard time covering expenses with my income gone.

The policy didn’t need to create a large inheritance or solve every possible financial problem. It was meant to protect against a specific and temporary vulnerability.

I didn’t need to buy a permanent policy with an LTC rider, because I already had an outstanding legacy LTC policy that provides excellent coverage at low cost, far better than anything available in the market today.

That experience crystallized how I think about life insurance.

I don’t think about buying life insurance in the abstract. Instead, I ask a much narrower question: What financial risk am I trying to address, and is a life insurance policy the right way to do so?

For many retirees, the fear that drives life insurance decisions is the risk of leaving a surviving spouse financially vulnerable after decades spent building stability together.

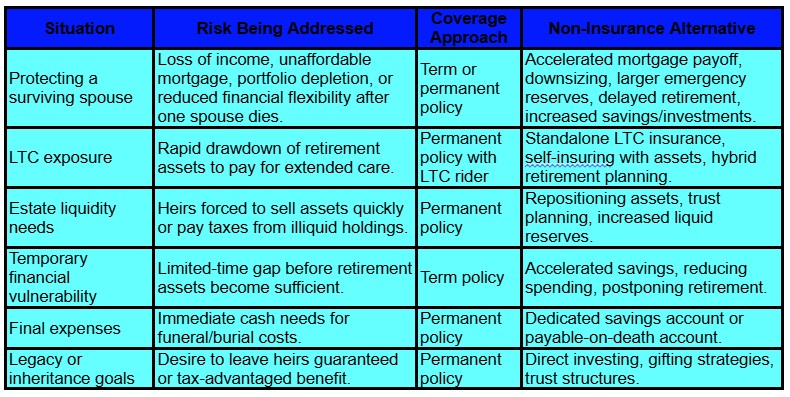

Table 2 lists a range of situations where life insurance may be helpful, but also suggests non-insurance alternative solutions.

How to Decide If Life Insurance Is Right for You as a Senior

As you can see, insurance can be a helpful solution, but it’s not the only possible tool.

Sometimes it’s the right tool, other times it isn’t.

The right answer for you, personally, depends on the size of the risk you’re trying to address, the likelihood of it occurring, your existing resources, and whether the premium cost makes sense compared to your other options.

The question to ask isn’t whether life insurance for seniors is universally good or bad.

It’s deciding if, in your situation, it’s an overpriced solution to a relatively minor concern, or a possibly expensive, but still cost-effective solution to a potentially catastrophic problem, and one that’s hard to accomplish through alternate means.

This change in how you think about it can make the decision much less confusing.

Before you decide to buy such insurance, answer these questions, preferably with your financial advisor, if you have one.

- How much will such a policy cost over time, and is this cost affordable to me?

- What specific financial risk would this policy address?

- Who would be financially impacted if I died tomorrow, and what would happen to them if I did nothing?

- Is this risk permanent or temporary, and if the latter, how long will it persist?

- Do I already have adequate protection through other means?

- Is insurance the most cost-effective solution to this problem or are there better alternative solutions?

- If I already own coverage, what changes if I keep it vs. cancel it?

Answering these questions won’t completely eliminate uncertainty, but it should help separate financially grounded considerations from emotional factors, and make your decision much clearer.

Singh explains, “The three factors I weigh most heavily when considering if life insurance makes sense are estate liquidity needs, LTC risk exposure, and the tax character of assets being passed to heirs. Emotional factors like legacy and not being a burden are real and valid, but they need to be grounded in an actual financial structure, otherwise the policy becomes a feel-good expense.

“When considering term vs. permanent policies for seniors, term rarely makes sense unless there’s a specific short-horizon need like covering a business obligation or a mortgage. In most cases I recommend permanent coverage, specifically because of the LTC rider option, the level premium structure, and the estate planning utility. The death benefit becoming a tax-free asset for heirs is a meaningful advantage when the alternative is leaving a pre-tax IRA subject to the 10-year distribution rule under the SECURE Act.”

Kusmider agrees and suggests, “Start with the need. Who is financially impacted if you die, and by how much? Key factors are protecting a spouse’s income, paying off debts, and covering final expenses (often $15,000+, depending on location). Emotionally, many seniors want to avoid becoming a burden, but the best solution is the one that protects family without jeopardizing the senior’s own financial stability.

“Term policies can be ideal when the need is temporary, for example, a 10-year bridge to cover a mortgage or income gap, if the senior can qualify and the term is available at their age. Permanent options (whole life / final expense / guaranteed issue) are usually for lifetime needs like burial costs or a small legacy, but they cost more and guaranteed-issue/final-expense policies often come with graded benefit tradeoffs.”

The Bottom Line: Life Insurance for Seniors Is a Tool, Not a Default

Life insurance for seniors is neither universally wise nor universally wasteful.

For some seniors, it may offer little value beyond providing reassurance, while wasting income that could make retirement more comfortable.

As Singh says, “There are times when life insurance doesn’t make sense. If a client has ample liquid assets, no estate liquidity problem, no LTC exposure concern, and heirs who have no meaningful tax burden to manage, there’s no problem for the policy to solve. Paying premiums in that situation is just cost without purpose.”

For other seniors, it may help protect a spouse, preserve assets during an LTC crisis, create estate liquidity, or mitigate a temporary but significant financial risk.

Your goal shouldn’t be to maximize coverage. That can leave you paying for coverage that does little beyond generating agent commissions and insurer profits.

Instead, you want to make sure any policy you’re considering addresses real financial risks that still matter, and does so more cost-effectively than possible alternatives.

Kusmider shares, “I always ask folks seeking insurance, ‘Why? What brought you to this conversation?’ If they live another 10–20 years, will the total premiums still be worth the benefit? If the ‘why’ is clear and the math aligns, coverage can help. If not, it can be a costly mistake.”

Singh agrees, “One question I wish every senior would ask is, ‘What specific financial problem does this policy solve?’ If the answer is vague, that’s a signal to pause. Life insurance is a powerful tool when there’s a clear problem. Without such a problem, it is just an expense.”

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher